All Categories

Featured

Table of Contents

If you pick degree term life insurance, you can allocate your costs because they'll remain the exact same throughout your term. And also, you'll recognize specifically just how much of a survivor benefit your recipients will obtain if you pass away, as this amount will not change either. The prices for level term life insurance will certainly rely on numerous factors, like your age, health and wellness condition, and the insurance provider you choose.

When you go through the application and clinical test, the life insurance coverage firm will assess your application. Upon authorization, you can pay your very first costs and sign any type of pertinent documentation to ensure you're covered.

You can choose a 10, 20, or 30 year term and enjoy the added tranquility of mind you are worthy of. Working with an agent can assist you find a plan that works best for your needs.

As you seek ways to protect your monetary future, you have actually most likely stumbled upon a variety of life insurance policy options. term vs universal life insurance. Selecting the appropriate protection is a large decision. You want to discover something that will certainly help sustain your enjoyed ones or the reasons essential to you if something happens to you

Lots of people lean towards term life insurance policy for its simpleness and cost-effectiveness. Term insurance policy contracts are for a fairly brief, defined time period but have choices you can customize to your needs. Certain advantage alternatives can make your costs alter gradually. Degree term insurance coverage, nonetheless, is a kind of term life insurance policy that has regular settlements and an unchanging.

Expert A Renewable Term Life Insurance Policy Can Be Renewed

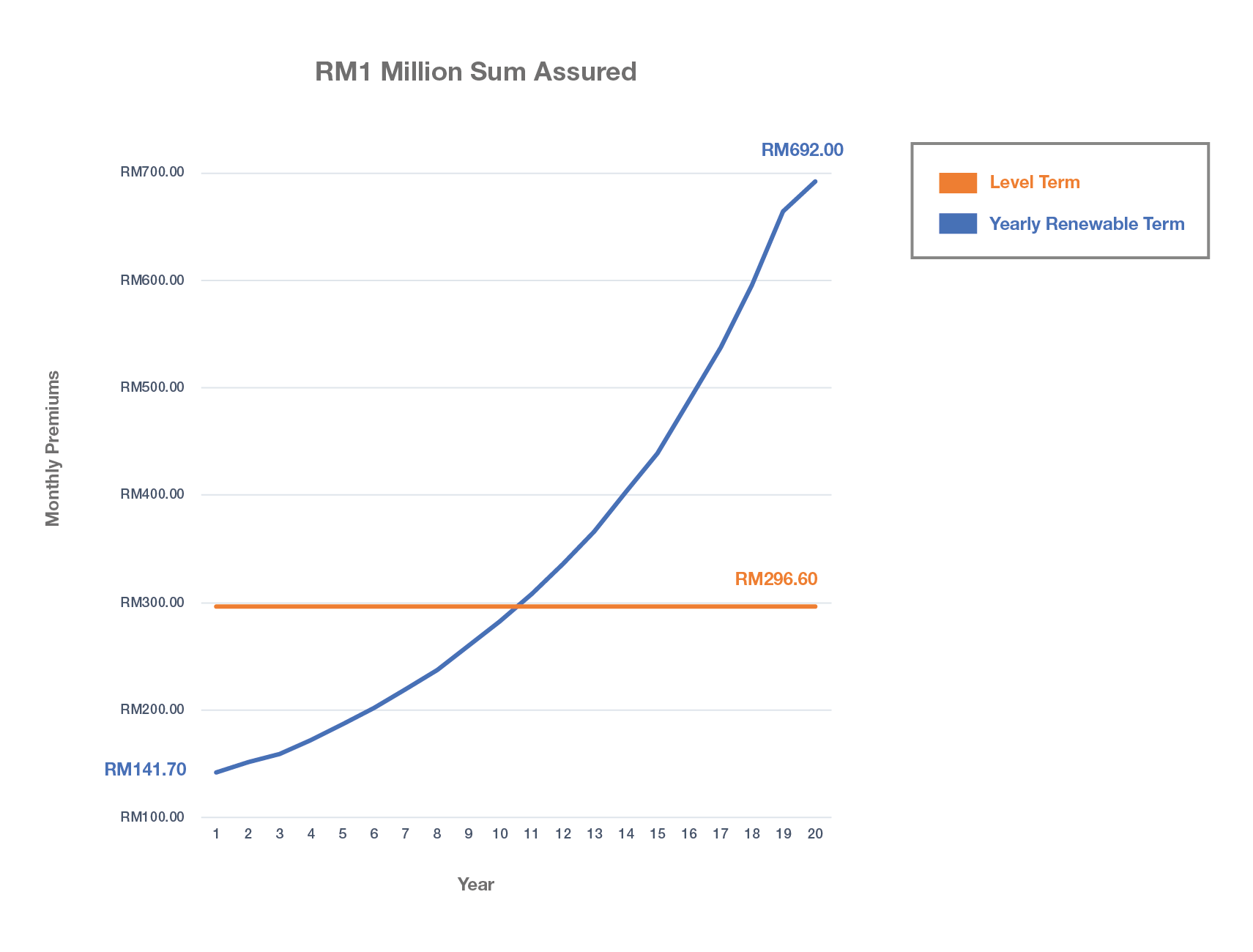

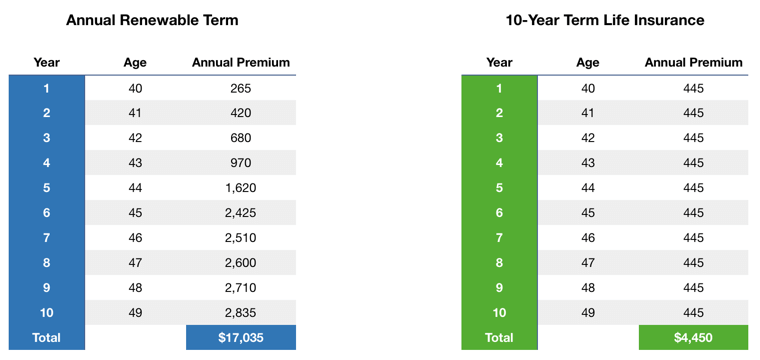

Level term life insurance is a subset of It's called "degree" due to the fact that your premiums and the advantage to be paid to your liked ones stay the same throughout the agreement. You will not see any type of changes in price or be left asking yourself about its value. Some contracts, such as every year renewable term, may be structured with costs that enhance over time as the insured ages.

Fixed death advantage. This is also set at the start, so you can know specifically what fatality benefit amount your can anticipate when you die, as long as you're covered and current on premiums.

This usually between 10 and thirty years. You consent to a fixed costs and survivor benefit throughout of the term. If you die while covered, your fatality advantage will be paid to enjoyed ones (as long as your costs are up to date). Your recipients will know in advance exactly how a lot they'll get, which can help for intending objectives and bring them some monetary safety and security.

You may have the option to for an additional term or, more most likely, restore it year to year. If your agreement has an assured renewability provision, you may not require to have a new medical examination to keep your coverage going. Nonetheless, your costs are most likely to increase due to the fact that they'll be based on your age at renewal time (joint term life insurance).

With this choice, you can that will certainly last the remainder of your life. In this case, once more, you might not need to have any kind of brand-new clinical exams, yet costs likely will increase as a result of your age and new insurance coverage. increasing term life insurance. Different firms offer numerous choices for conversion, be sure to understand your choices before taking this action

Coverage-Focused Level Term Life Insurance

Many term life insurance coverage is level term for the period of the agreement period, but not all. With decreasing term life insurance coverage, your fatality advantage goes down over time (this kind is usually taken out to specifically cover a lasting debt you're paying off).

And if you're established up for renewable term life, then your costs likely will go up every year. If you're exploring term life insurance policy and desire to make certain simple and foreseeable economic security for your family members, level term might be something to think about. As with any type of kind of insurance coverage, it might have some constraints that don't meet your requirements.

Tailored Level Term Life Insurance Meaning

Usually, term life insurance coverage is a lot more budget friendly than long-term insurance coverage, so it's a cost-efficient means to protect monetary defense. At the end of your agreement's term, you have numerous options to proceed or relocate on from insurance coverage, often without requiring a clinical exam.

Just like other sort of term life insurance policy, as soon as the agreement finishes, you'll likely pay greater costs for insurance coverage since it will certainly recalculate at your existing age and health. Fixed protection. Degree term offers predictability. If your monetary circumstance adjustments, you may not have the needed coverage and might have to purchase additional insurance policy.

Yet that doesn't mean it's a suitable for every person. As you're buying life insurance coverage, right here are a few key factors to consider: Spending plan. One of the benefits of degree term protection is you know the expense and the fatality advantage upfront, making it simpler to without fretting about boosts over time.

Typically, with life insurance coverage, the healthier and more youthful you are, the more affordable the coverage. If you're young and healthy and balanced, it may be an enticing option to secure in low costs currently. If you have a young family, for instance, level term can help give financial support throughout important years without paying for insurance coverage much longer than required.

1 All riders are subject to the terms and problems of the rider. Some states might differ the terms and conditions.

2 A conversion credit score is not offered for TermOne policies. 3 See Term Conversions section of the Term Collection 160 Product Overview for how the term conversion credit score is determined. A conversion credit score is not offered if premiums or costs for the brand-new policy will be forgoed under the terms of a rider supplying disability waiver advantages.

Decreasing Term Life Insurance

Term Collection items are issued by Equitable Financial Life Insurance Firm (Equitable Financial) (NY, NY) and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Policy Agency of California, LLC in CA; Equitable Network Insurance Coverage Company of Utah in UT; and Equitable Network of Puerto Rico, Inc. Term Life Insurance is a kind of life insurance plan that covers the insurance holder for a specific amount of time, which is known as the term. Terms commonly range from 10 to 30 years and rise in 5-year increments, giving level term insurance policy.

{kind=link}

Latest Posts

Tax-Free What Is Level Term Life Insurance

Voluntary Term Life Insurance

Honest Direct Term Life Insurance Meaning