All Categories

Featured

Table of Contents

That usually makes them a much more budget friendly option for life insurance policy protection. Some term plans may not keep the premium and fatality profit the same gradually. You don't intend to incorrectly believe you're getting degree term protection and then have your death benefit adjustment later. Numerous individuals get life insurance policy protection to help financially protect their liked ones in case of their unanticipated death.

Or you might have the alternative to convert your existing term protection into a long-term policy that lasts the remainder of your life. Different life insurance coverage policies have prospective benefits and drawbacks, so it's important to understand each prior to you choose to buy a plan.

As long as you pay the costs, your beneficiaries will certainly receive the survivor benefit if you die while covered. That claimed, it's crucial to note that a lot of plans are contestable for 2 years which indicates insurance coverage might be retracted on fatality, needs to a misstatement be found in the application. Policies that are not contestable commonly have actually a graded survivor benefit.

Premiums are usually reduced than entire life policies. You're not locked right into a contract for the rest of your life.

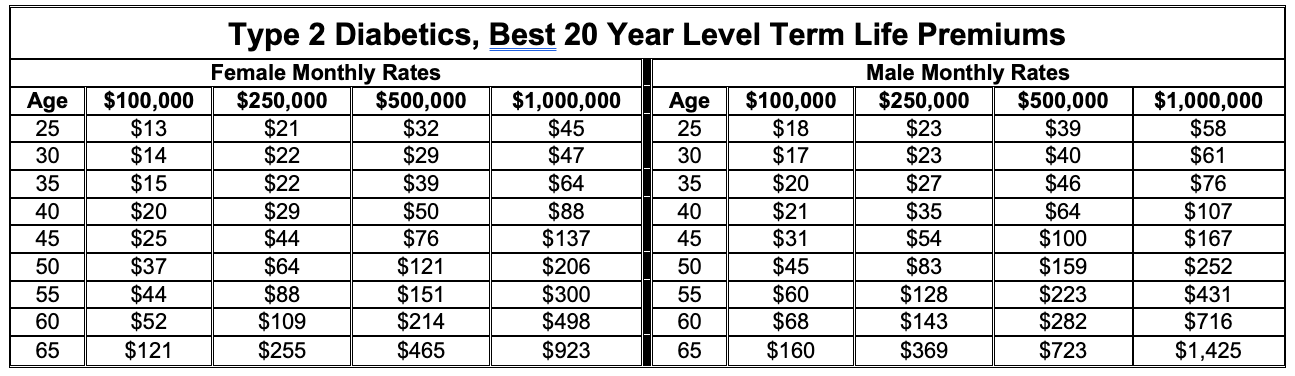

And you can't pay out your plan during its term, so you will not obtain any kind of financial benefit from your past protection. Similar to other kinds of life insurance coverage, the expense of a level term policy depends on your age, insurance coverage demands, employment, way of life and wellness. Usually, you'll discover extra budget-friendly insurance coverage if you're more youthful, healthier and less dangerous to guarantee.

Proven Term To 100 Life Insurance

Since degree term costs stay the same for the duration of insurance coverage, you'll know precisely how much you'll pay each time. Level term coverage also has some adaptability, allowing you to customize your plan with additional features.

You might have to meet certain conditions and certifications for your insurer to enact this cyclist. There likewise can be an age or time restriction on the insurance coverage.

The survivor benefit is usually smaller sized, and coverage usually lasts until your child turns 18 or 25. This cyclist might be a much more cost-effective way to aid ensure your youngsters are covered as cyclists can commonly cover numerous dependents at as soon as. Once your child ages out of this coverage, it might be feasible to convert the cyclist into a new plan.

When comparing term versus long-term life insurance policy. guaranteed issue term life insurance, it is very important to remember there are a few different types. One of the most common kind of long-term life insurance policy is entire life insurance policy, but it has some key distinctions compared to level term insurance coverage. Here's a basic introduction of what to think about when contrasting term vs.

Whole life insurance policy lasts for life, while term protection lasts for a particular period. The costs for term life insurance policy are typically less than entire life insurance coverage. With both, the premiums stay the very same for the duration of the plan. Entire life insurance policy has a money worth part, where a section of the costs may expand tax-deferred for future needs.

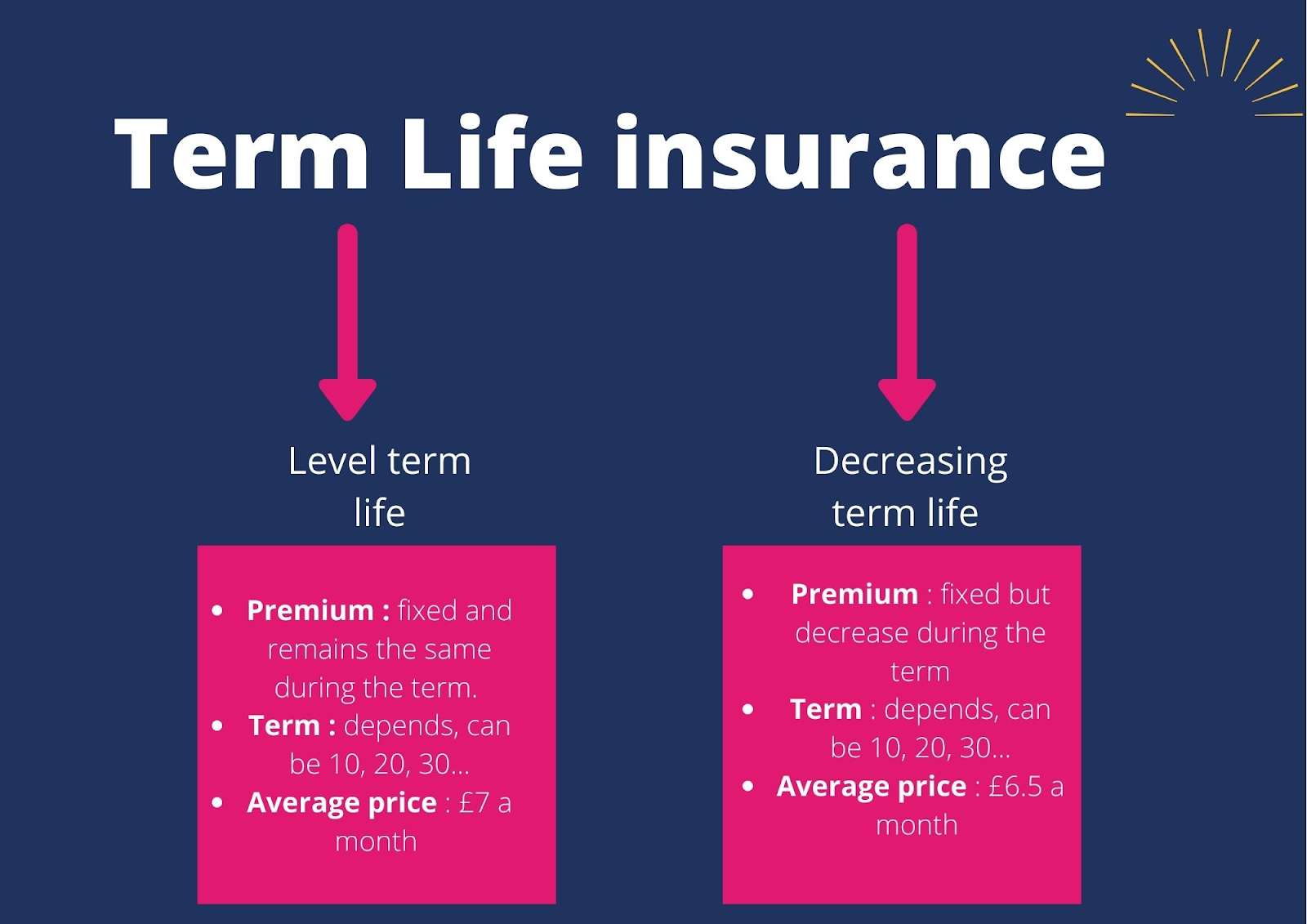

One of the primary features of level term coverage is that your premiums and your death advantage don't alter. You might have coverage that begins with a fatality benefit of $10,000, which could cover a home mortgage, and after that each year, the death advantage will lower by a set quantity or percent.

Due to this, it's often a more economical type of level term insurance coverage., yet it may not be enough life insurance coverage for your requirements.

After choosing on a policy, finish the application. If you're accepted, authorize the paperwork and pay your very first premium.

Secure What Is Voluntary Term Life Insurance

Ultimately, consider organizing time annually to assess your plan. You may intend to upgrade your recipient details if you've had any considerable life modifications, such as a marriage, birth or separation. Life insurance can in some cases feel difficult. But you do not have to go it alone. As you explore your alternatives, consider reviewing your needs, wants and worries with a financial expert.

No, level term life insurance does not have money value. Some life insurance policy policies have a financial investment attribute that allows you to build cash worth gradually. A section of your costs payments is established apart and can make passion in time, which grows tax-deferred during the life of your insurance coverage.

You have some alternatives if you still desire some life insurance coverage. You can: If you're 65 and your coverage has run out, for instance, you might want to buy a brand-new 10-year degree term life insurance coverage policy.

Family Protection Level Term Life Insurance

You might be able to convert your term protection into a whole life policy that will certainly last for the remainder of your life. Lots of kinds of level term policies are convertible. That indicates, at the end of your coverage, you can convert some or all of your policy to entire life protection.

Degree term life insurance policy is a policy that lasts a collection term normally between 10 and 30 years and comes with a level survivor benefit and degree costs that remain the same for the whole time the plan is in impact. This suggests you'll recognize precisely just how much your settlements are and when you'll have to make them, enabling you to budget appropriately.

Level term can be an excellent choice if you're looking to buy life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance Barometer Study, 30% of all adults in the U.S. demand life insurance policy and do not have any type of kind of policy. Degree term life is foreseeable and economical, which makes it one of the most preferred kinds of life insurance policy.

{kind=link}

Latest Posts

Final Expense Insurance Definition

United Funeral Directors Benefit Life Insurance Company

Globe Life Final Expense Insurance Reviews